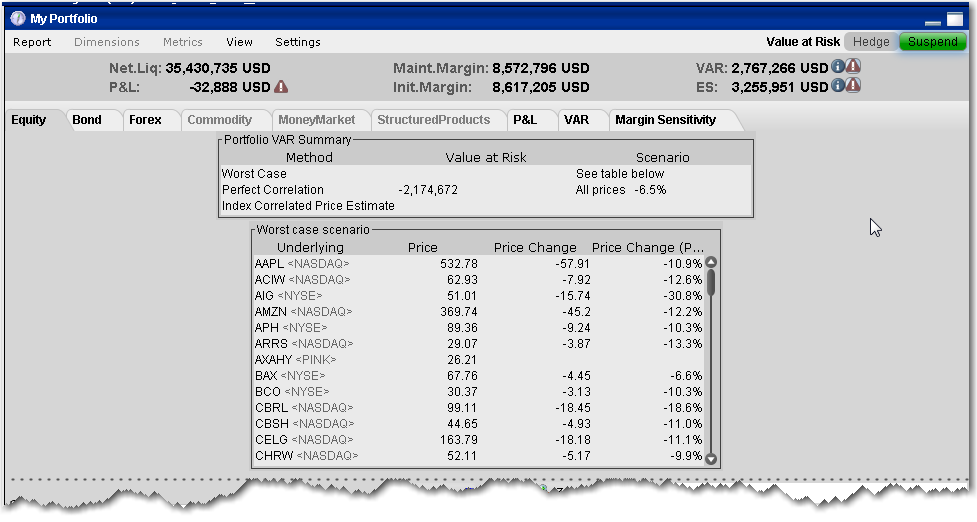

The Value at Risk report shows the greatest loss that a portfolio will sustain over a one-day period, with either 95%, 99.5% or 99.5% confidence. VAR is calculated using three different methods, each with different assumptions about correlations of the underlying assets in the portfolio. This report is only available in the Equity tab and is calculated in real-time using the P&L plot data. To see VAR for you entire portfolio, use the VAR tab.

1. Open the Risk Navigator.

- From Mosaic - Use the New Window drop down and select Risk Navigator from the Advanced Trading Tools category.

- From Classic TWS - Use the Analytical Tools menu and select Risk Navigator from the Portfolio category.

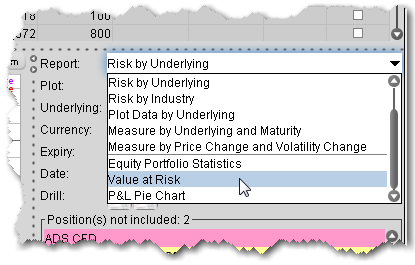

2. From the Report field, select Value at Risk.