The sensitivity of an individual stock to the movement in the broader market is known as its beta. Stocks sensitive to market movements typically have high betas over time. Stocks that show low correlation with the market have low betas, while some may move broadly in line with the market as a whole. Stocks that move inversely to the market would have negative betas.

Risk Navigator measures beta-weighted performance, allowing traders to consider risk by measuring individual component correlation with a market index in order to estimate likely gains or losses in the event of a given move in the market.

For the same portfolio of stocks, we can generate contrasting risk profiles by looking at risk units in delta-terms versus beta-terms, which shows the aggregate sensitivity of a portfolio to a market index.

You can find beta risk elements across the Risk Navigator:

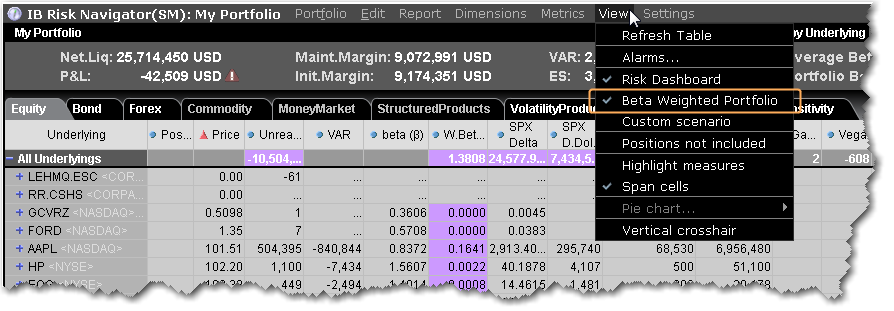

To enable Beta Weighting

Beta-weighting allows traders to contrast the likely performance of a delta neutral portfolio (should the component pieces behave in the future as they have in the past) with respect to a specific benchmark index or reference contract. One might expect a long high-beta portfolio to perform better when considering beta-weighting in the event of a market rise in comparison to its performance when assuming it is equally delta-weighted. Conversely, its beta-weighted performance should be expected to be worse for a market fall in comparison to an across the board equal-weighted decline for all component pieces.