Tax Information and Reporting - Wash Sales

TAX INFORMATION AND REPORTING

Wash Sales

Wash Sales: Understanding the Basics

The wash sales rule was implemented to defer the deduction when a taxpayer sells a security at a loss and purchases the same or an equivalent security within a short period of time. A sale of stock or securities is considered a "wash sale" if a trader sells shares or securities at a loss and purchases the same or equivalent shares or securities within the 61-day wash sale period, which includes the 30 calendar days before the sale, the day of the sale, and 30 calendar days following the sale.

When the loss on the sale is deferred, the amount of the loss is added to the cost basis of shares purchased during the wash sale period ("replacement shares"). Upon the sale of the replacement shares, the disallowed loss is incorporated into the calculations of the gain or loss on the replacement shares and recognized. Additionally, the holding period of the original shares is added to the holding period of the newly acquired shares or securities.

Wash sale rules apply to losses from short sales, securities options and securities futures. They do not apply to losses from commodity contracts or foreign currencies.

Wash Sales and Activity Statements

Interactive Brokers includes wash sales on daily, monthly and annual Activity Statements for all 1099-eligible accounts, as required by the IRS. Our wash sales are calculated on a granular basis, in other words as the shares actually trade through the system. This may result in multiple wash sales which at the end of a day sum to zero impact. Note however that there may be a timing difference with year-end recognition impacting the annual statement.

Tax reporting for Wash Sales

Beginning in 2011 losses disallowed due to wash sales are reported to the IRS on securities purchased and sold after January 1, 2011. Please refer to the sections on 1099B reporting and form 8949 for more information.

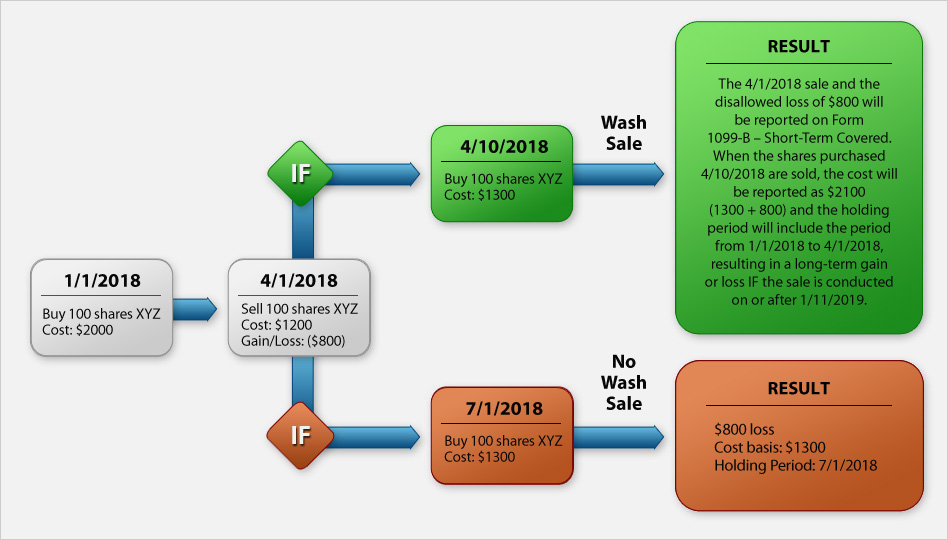

Example

The example below shows a series of transactions that differ only in the purchase date of the last trade. One transaction triggers a wash sale, the other does not. This example also shows how the disallowed loss is added to the cost basis of the newly purchased replacement shares.

Note:

IRS Circular 230 Notice: These statements are provided for information purposes only, are not intended to constitute tax advice which may be relied upon to avoid penalties under any federal, state, local or other tax statutes or regulations, and do not resolve any tax issues in your favor.